first time home buyers

-

·

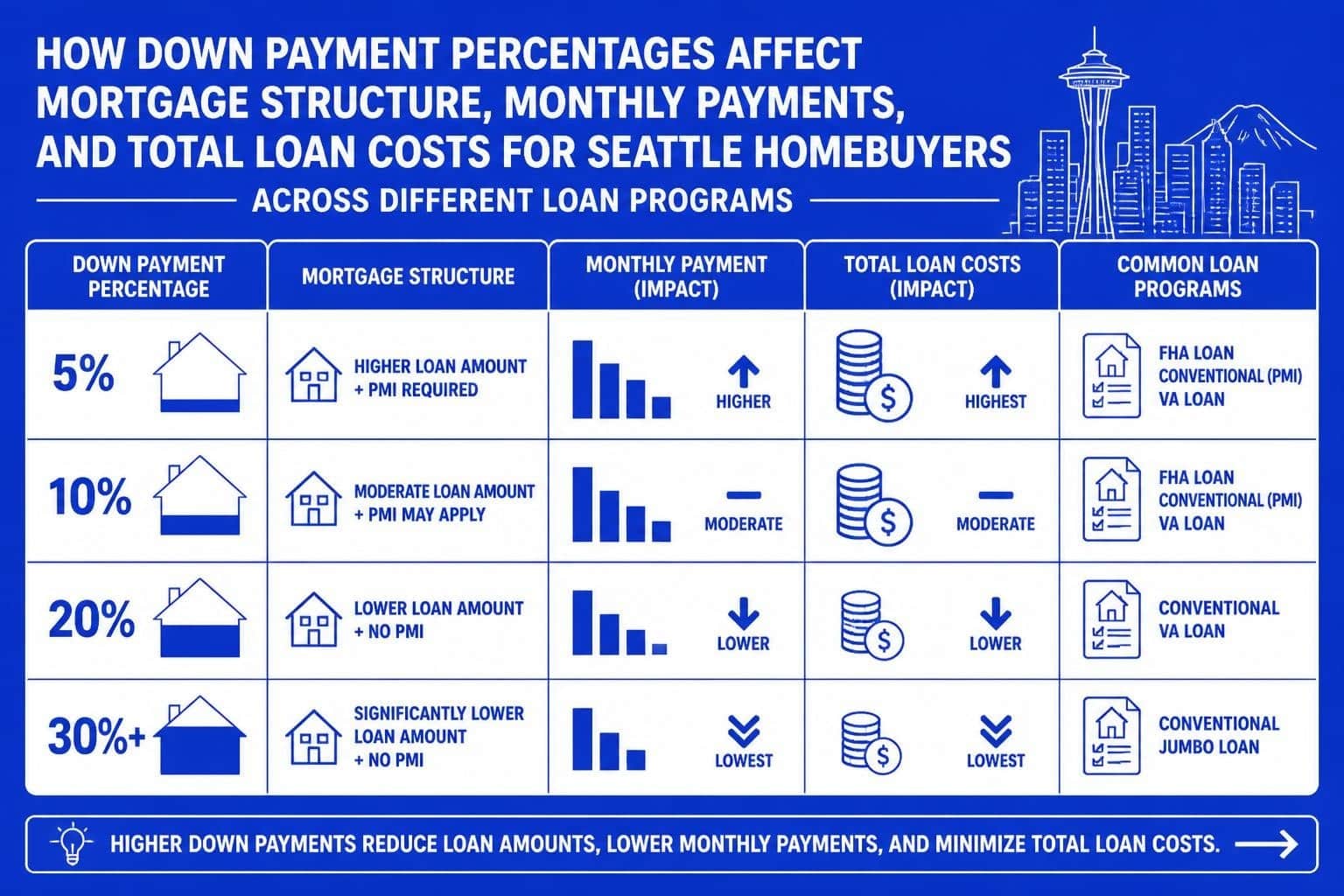

Down Payment and Mortgage Guide for Seattle Homebuyers

Expert guide to down payment and mortgage planning in Seattle. Learn requirements, strategies, and how…

-

·

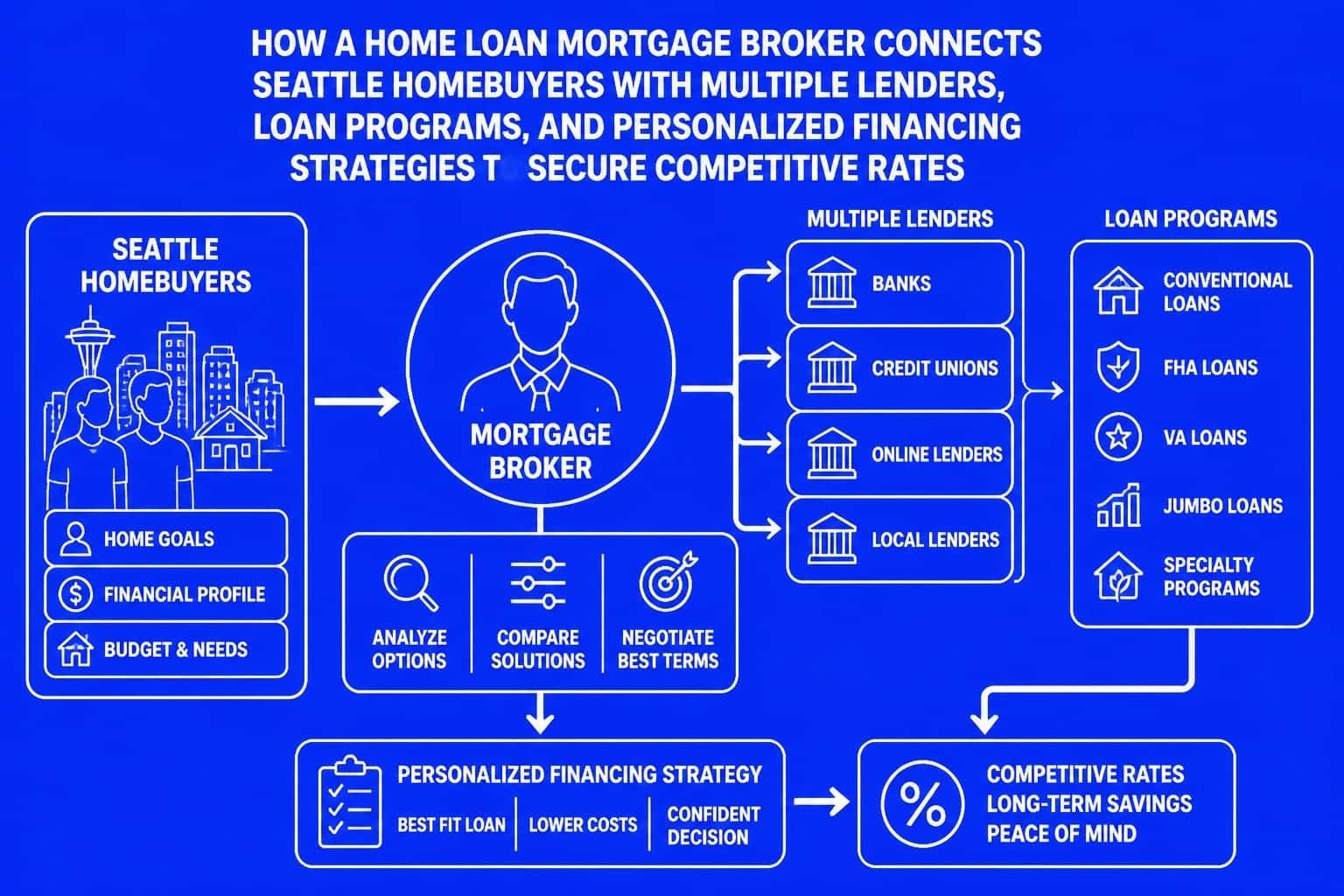

Home Loan Mortgage Broker Guide for Seattle Buyers

Discover how a home loan mortgage broker helps Seattle homebuyers navigate purchase and refinance options…

-

·

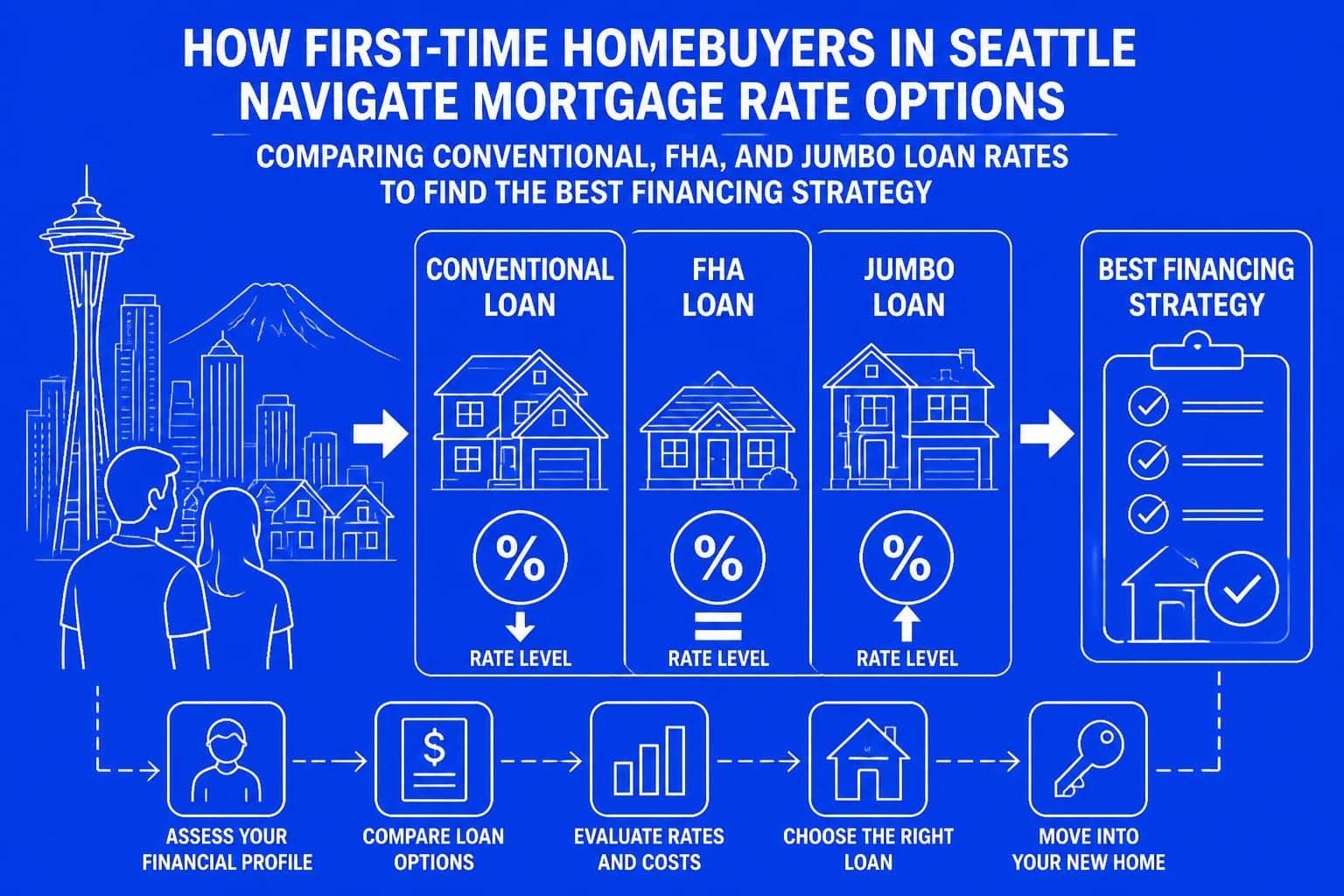

First Time Mortgage Rates in Seattle: 2026 Guide

Understand first time mortgage rates in Seattle. Expert insights on qualifying, loan options, and strategies…

-

·

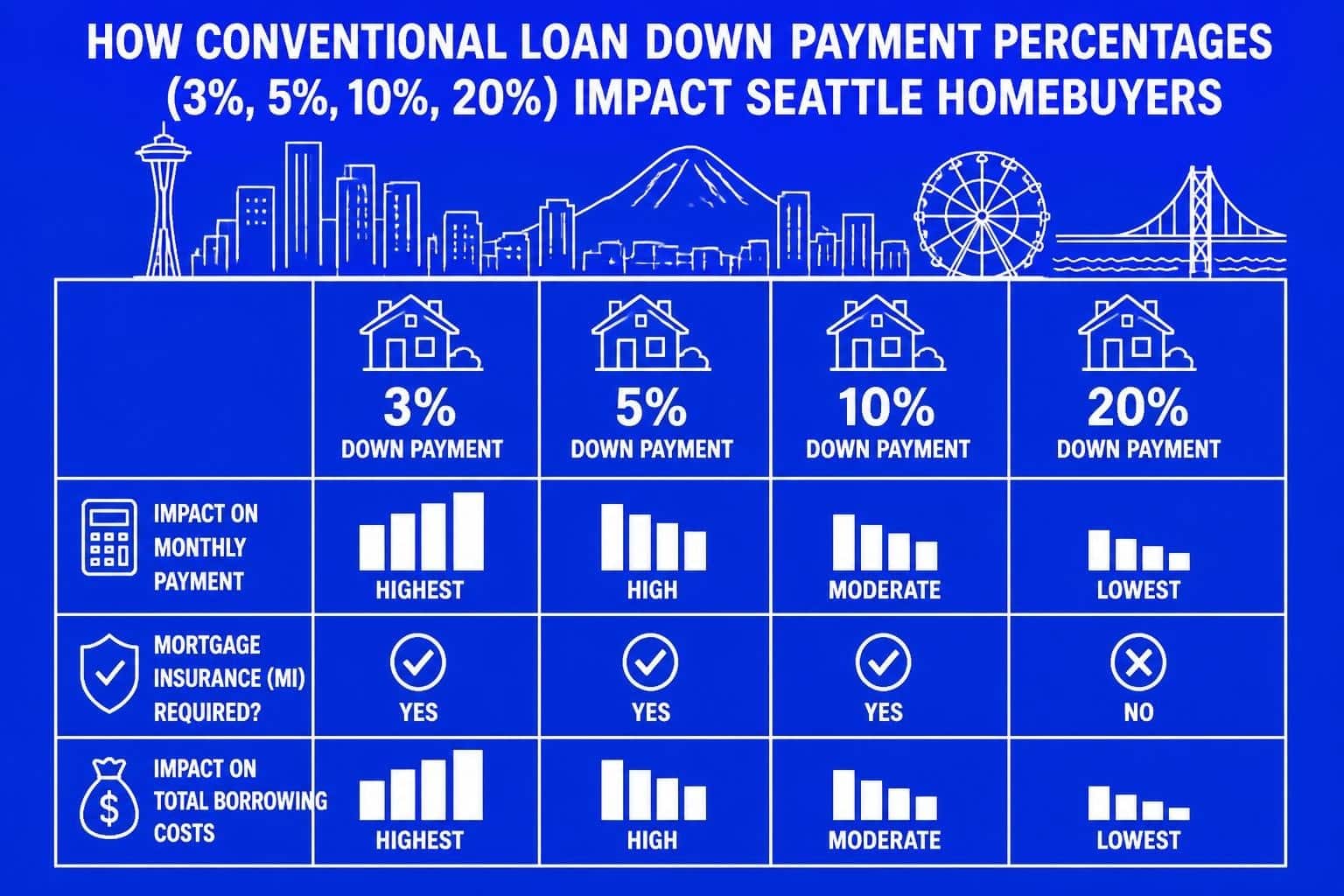

Conventional Loans Down Payment in Seattle (2026 Guide)

Learn conventional loans down payment requirements in Seattle. Expert guide covering 3%, 5%, and 20%…

Get Your Rate Quote

Please provide the following information to receive your personalized mortgage rate