seattle mortgage reel

-

·

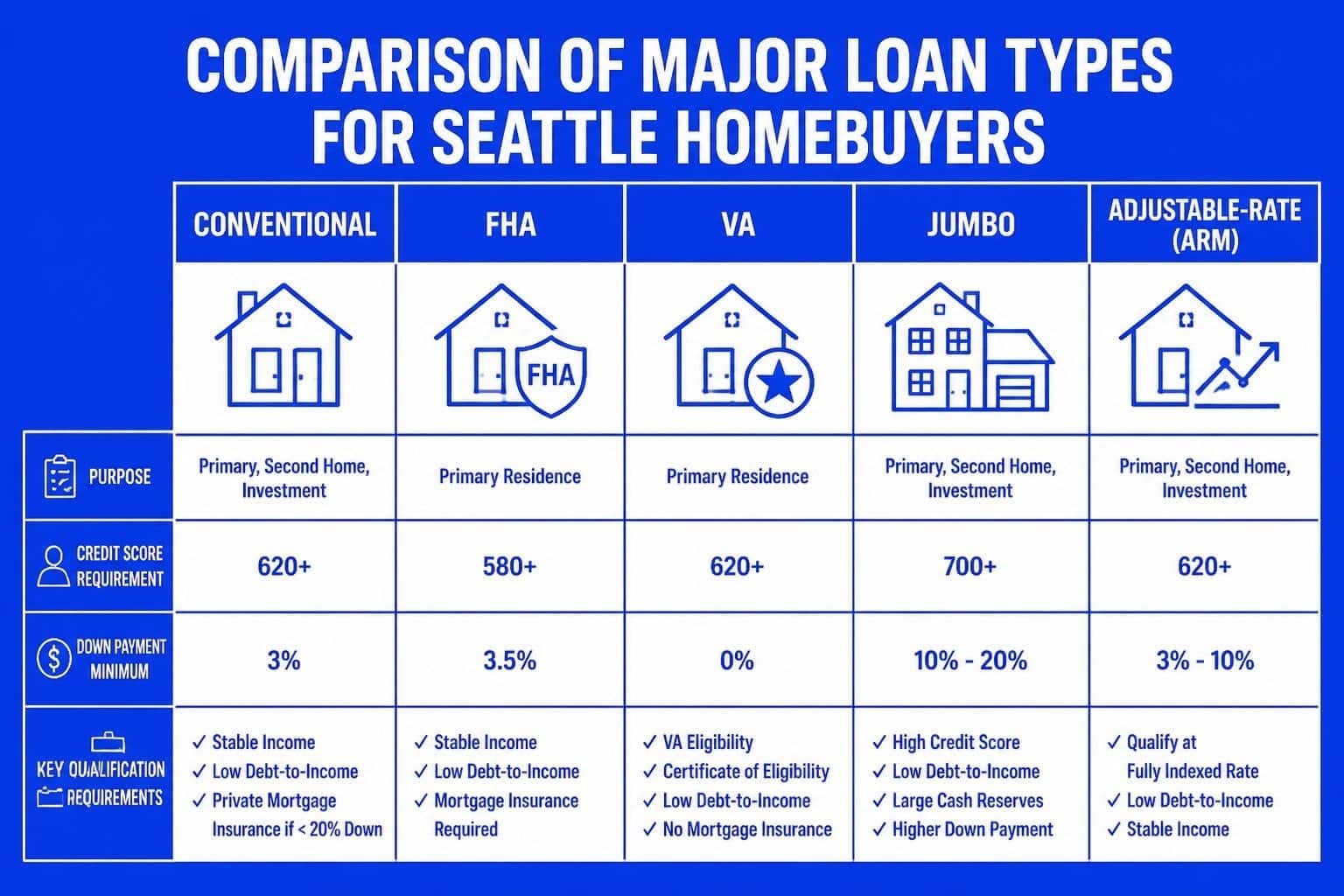

Loan Types Mortgage: A Seattle Homebuyer’s Complete Guide

Explore loan types mortgage options in Seattle. From conventional to jumbo loans, learn which mortgage…

-

·

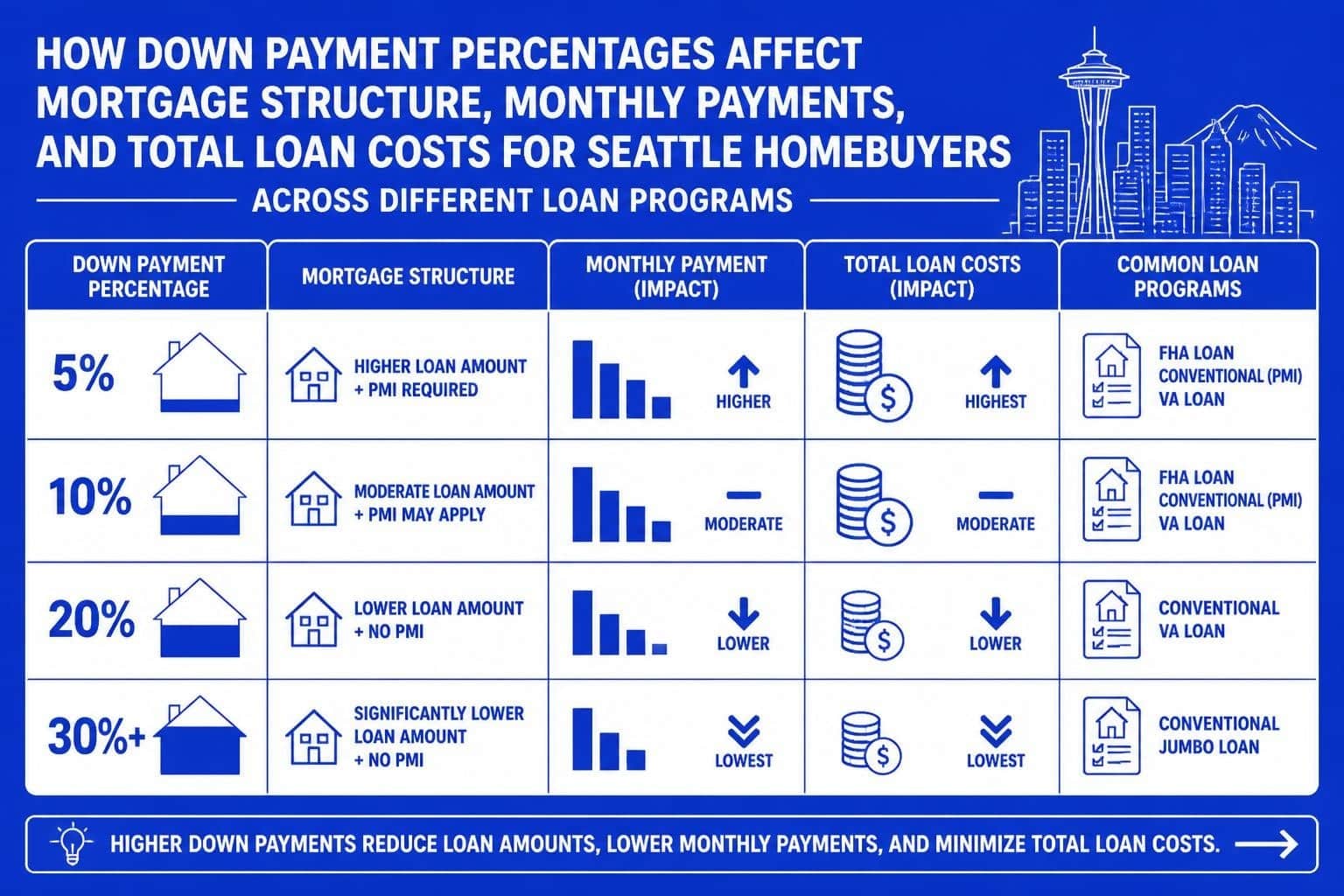

Down Payment and Mortgage Guide for Seattle Homebuyers

Expert guide to down payment and mortgage planning in Seattle. Learn requirements, strategies, and how…

-

·

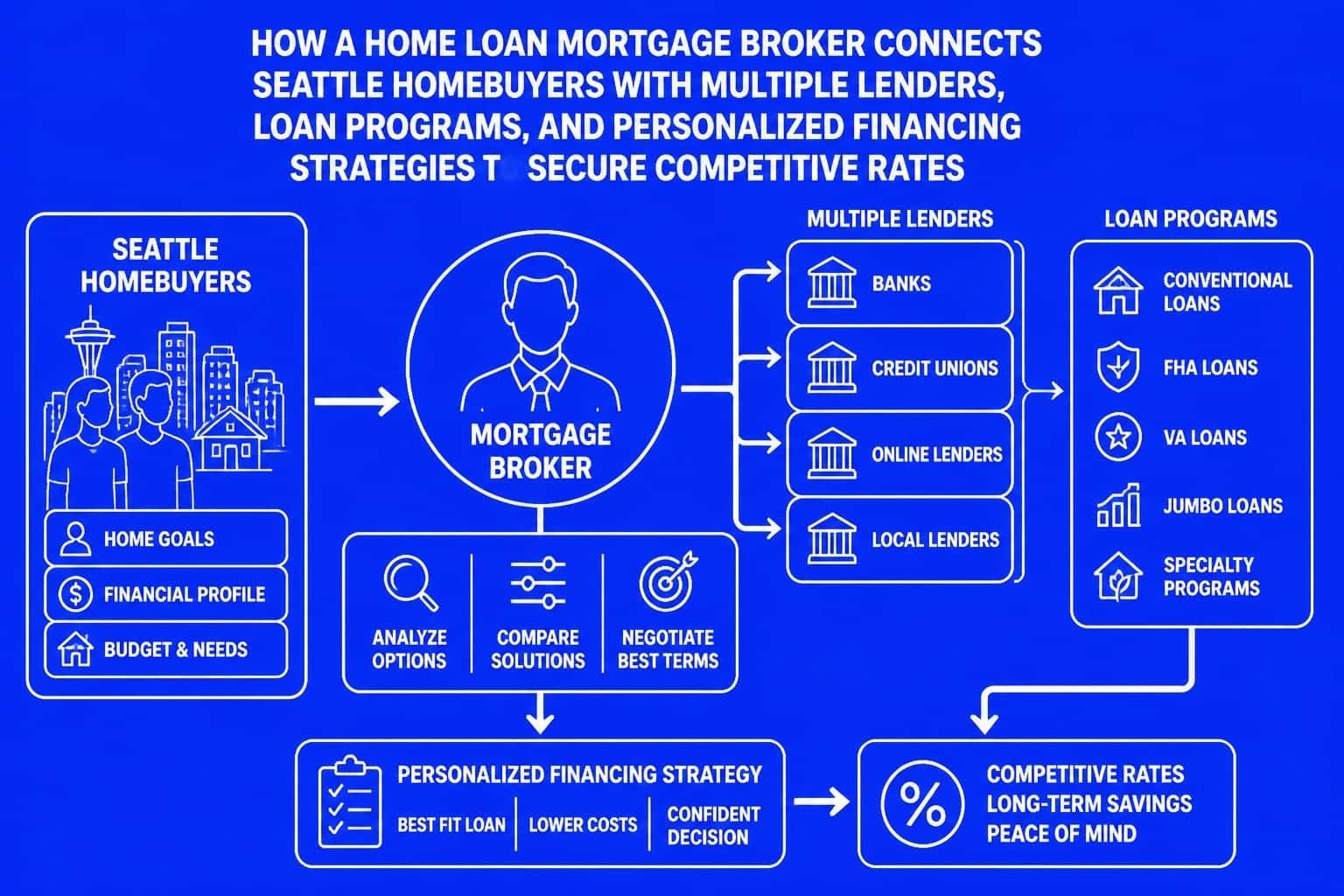

Home Loan Mortgage Broker Guide for Seattle Buyers

Discover how a home loan mortgage broker helps Seattle homebuyers navigate purchase and refinance options…

-

·

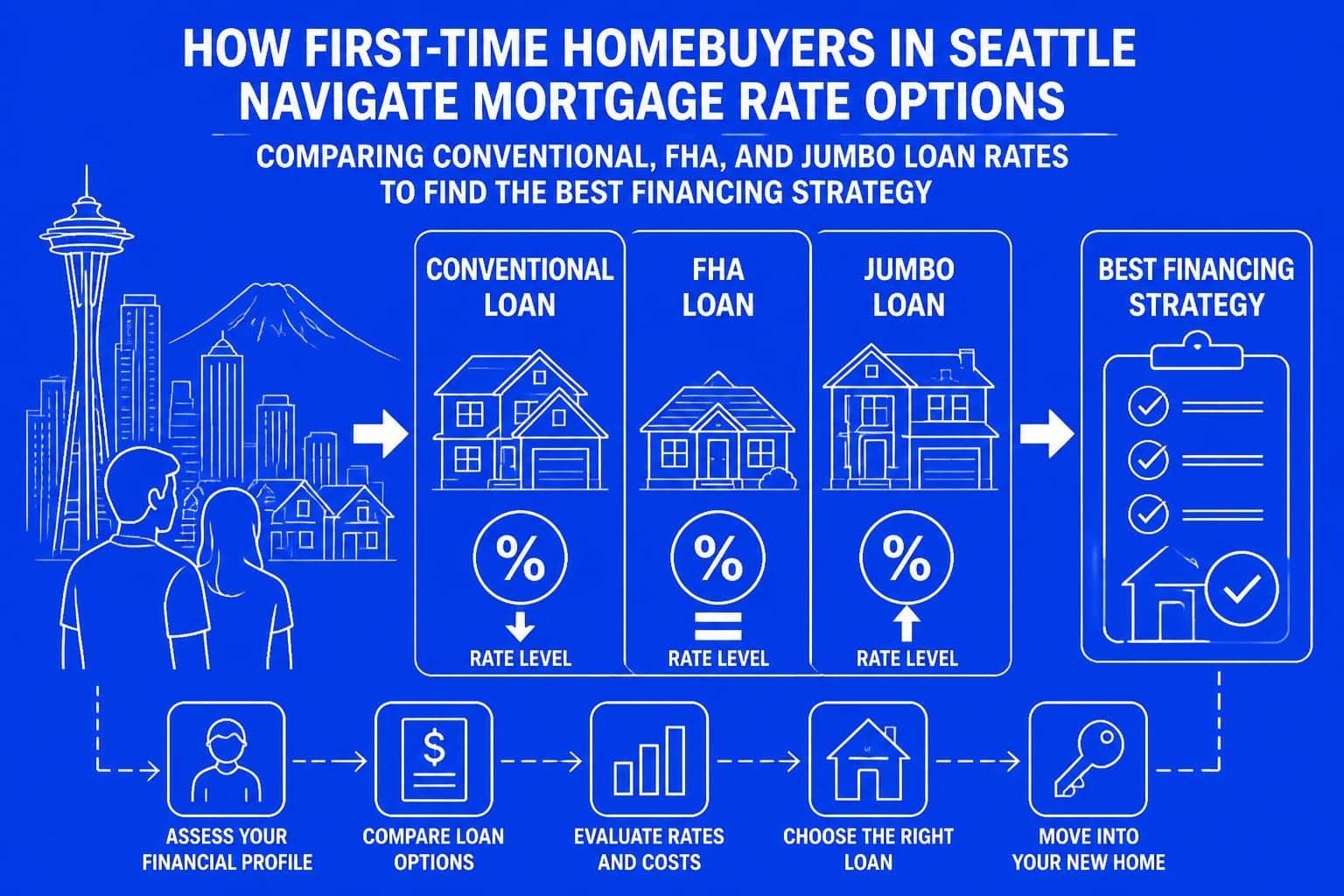

First Time Mortgage Rates in Seattle: 2026 Guide

Understand first time mortgage rates in Seattle. Expert insights on qualifying, loan options, and strategies…

Get Your Rate Quote

Please provide the following information to receive your personalized mortgage rate